This is the 2nd post in an ongoing exchange between myself and Graham Wright of Man Against The State. Graham’s first post takes the form of a line-by-line critique of the short presentation “Firing Back” from January 2012. The original video in question is here. All posts in this series are tagged “Graham Wright and Ben McLeish” for ease of calling up the series.

Graham’s post is of extreme length, and indeed fertile ground for an exposition of both his and my position, and as such I find myself in an awkward position of having to divide my response into two sections. I will spend the length of this piece clarifying and defending the ideas I so briefly had to cram into the video to which his critique is geared. Many of Graham’s misunderstandings are therefore not entirely his fault – and indeed, a central understanding of our movement is that human beings are only as able to be rational, as the quality of the information open to them. With that in mind I offer this refinement of my points to help him, and myself, in coming to terms with the various ideas presented by me, and by him.

I respond here in a fashion meant to address as many points as possible with perhaps a little less more brevity. However, anything that Graham deems of vital importance to address, which I do not, can be added in later posts, or even edited into this piece after the fact. Where I end up doing so, I will note that I have, for sake of clarity and intellectual honesty.

The second part of this missive will be the explanation of the functions and attributes of a Resource Based Economy. As such I warn my readers that if they are looking for a front-to-back characterization of this model, they will find it only in part here, as the elements that form part of the overall train of thought emerge within my rebuttals.

What is “Money”?

Graham begins his post with a fair point – I lack an overall definition of what money means. To resolve the accusation of a perpetrating a fallacy (an indulgence to which, as we shall see in a moment, Graham himself is no stranger) let me attempt an explanation here. It may be that we are already looking at a paragraph that will undergo some additions with the help of Graham. Anything to get us on the same page.

Money is, and has been throughout its relatively short history in the human story, a societal tool to facilitate the differential exchange value of property or human/machine labour (or property whose own value has been enhanced or modified by human or mechanical labour.)

In plain English, money is what the baker and the tailor can use as third-party exchange token because “one suit does not equal one loaf of bread.” Rather than exchange one suit for ten loaves of bread every time, and risk inconvenience or spoiling (an attribute to which we shall return very shortly) a granularity of exchange is enabled, whereby both parties can engage in the buying or selling of goods or services at a ratio of something other than 10-1.

What has been used as money? In addition to the fractional and fiat currency explained in “Firing Back”, and in a longer video from 2010 called The Future of Economics, much else has been used in the past as a medium of exchange. The most famous objects used are the “precious metals” of gold and silver, but also marijuana, chocolate, stones, ornamental belts in China and many others have been used at various times.

Money and Private Property

This overall description of money is a simplistic characterisation, however, and itself requires an additional explanation of how money has been framed in the philosophy of private property. Indeed, it is this framing that has ultimately given rise to two major issues with the monetary system. 1) Money has itself become a form of private property itself, and 2) it has become entirely decoupled from any real-world referent whatsoever, resulting in the overall separation of the operation of ANY definition of a market economy from its real world resource allocations, as well as its effects upon the life economy of the planet, what today’s corporate Newspeak characterises as “externalities.”

In fact the blurring of this line began with John Locke in his 1688 Two Treatises on Government, which sought to define” private property” as needing three characteristics in order to be considered legal and valid;

1) One needed to mix one’s labour with what one has appropriated from nature.

2) “Enough in good and common” should be enough left over for others to do the same with.

3) Whatever is being considered as property should not be left to “spoil.”

Seems reasonable enough, even if you don’t agree with Locke’s case per se. Then however, the work’s reasoning goes off, without warning, on an extreme logical tangent. Locke states that money invalidates all of these criteria now. After all, money-demand of individuals now buys the labour of (much more poor) others, hence labour itself is not a necessity for the justification of property any more. Money sates point 1. As for point 2, this is invalidated in a spurious pseudo-argument that since all members of society have accepted the use of money as a market-cultural logic, thus this “tacit” agreement satisfies the requirement of the plentiful nature of what is left over. As for Locke’s prior assertion that what is made private should not spoil – since money itself does not spoil, this is no longer an issue any more either!

What you’ll notice has just happened is that we have separated all referents to the operation of what Mises would term “human action” from actual real-life and real-world to the aggregation and leveraging of money-demand itself in their place. From this point onwards in history, 1688-now, no longer do the operating forces of any version of monetary policy take into account the basics of what was framed as “private property” in the real world to begin with. And you’ll also note the beginning of a thread which runs through from Locke to the present day, including Graham’s own arguments – namely, that there is an “irreducible complexity” to the market, an “invisible hand” to the order, or in Hayekian terms, “a transcendent order” to the whole game.

This will manifest itself in Graham’s writing in the form of the claim that, for example, millionaires must have rightfully earned their capital to begin with, and so the resulting leveraging of said money, be it for self-serving interest-bearing purposes or monopolistic or cartel-behaviour can be defended on this ground. Unfortunately, the Ur-genetics of this value set does not allow for this hopeful assertion. Money-ownership itself, and its concomitant in-built trumping of the requirement to avoid scarcity (Locke’s second point) or waste (his third) do not matter and are not vouchsafed by the conglomeration of money-demand into ever larger pools, with ever smaller memberships, at the expense of a growing underclass of anybody who happens to be born into a family which does not already control millions or billions, or increasingly, trillions of money tokens.

With which defined, I will move to Graham’s points.

Value

Graham has a problem with my defining money as being bestowed value by its scarcity (of the money supply, in this case) and its perceived shared value. He claims that since “value is subjective” this could be true of anything. Indeed – this is why many different items have been used as money in the past (even fairly spoilable ones.) Yet I am unsure how this argument is going to help him defend a monetary system. He then goes on to say that “fiat money’s value is not an illusion” – claiming that the rationale for this is that he “literally” can spend his fiat money on goods which have a life-use. There are a few problems with this:

1) He is about to admit that fiat money’s very definition is that it is itself useless as a product (same paragraph.)

2) I do establish in this talk that fiat money does not even have the backing of any “commodity money or useful resource – so we can’t use that as a basis either

3) Just because the exchange value is accepted in the culture does not make it “valuable” in the actual sense. The same could be said of the use of Pet Rocks in a monetary system, and it wouldn’t be any more true.

4) Even commodity money has fluctuating and relative values, again depending on people’s perception of its value.

We are already in an infinite regression loop here. Fiat money literally has value – then it does not. Commodity money does have a value (it has real-world uses) – but this fluctuates according to perceptions of its value. Hence it does not have a grounded definition of value implicit in it either, except based on its scarcity of supply or its perceived value – which, I am informed by Graham, are both questionable assertions of mine (of course they are not mine, but are, and consistently have been, claims of economists, including Hayek, in his Essay “A Free Market Monetary System” in which he describes several instances of increasing the value of gold and silver-backed economies by restricting the money supply.)

As a comic side-note; I have more than once been turned away from a checkout desk because I was holding a Scottish Ten Pound Note – and the cashier was unfamiliar with the note, and believed it to be invalid. No amount of arguing about its value got me my milk and eggs. Where’s the “value” in that? We may plead that ignorance of the note excuseth no man – but it does indeed underline the point that without faith in money it would be hard to come to a consensus about its value.

And before we hear claims that this would not be the case with commodity money; what use is gold? Why is it valuable? Indeed it shines, and is malleable. But what uses does it have? This sounds asinine, but the millions of tonnes of electronics wreckage in landfill, containing rare earth minerals and gold, testifies that we must be living in a world which appreciates only short-term, linear use value. And this is the key point of what The Zeitgeist Movement tries to express. We are wasting actual resources in a one-way consumption drive that would not be reversed by any form of monetary reform in the long run. It is a decoupled system of value-appreciation.

Moving onward (although I’m sure Graham and I will return to the above, and I will be happy to) – Graham points out the boom-bust cycle as a product of fractional reserve banking. He is entirely correct. I would add to this, that during busts, especially modern busts, like that of 1929 or 2008, MASSIVE redistribution of wealth aggregates to the top money-possesors. A rather large issue. Additionally, social life-systems are sold off at bargain basement prices (as in the UK’s NHS, or indeed Chile, Argentina, or modern day Greece.) But this is implicit in his paragraph. I dealt more closely with this in The Future of Economics. Graham’s points and mine shouldn’t be controversial – but in a system owned by the central banks, who also co-own, or own outright, the ever fewer and fewer media outlets, the logic that said system serves the central banks is wiped from discourse like a shaken etch-a-sketch.

Interest is Not Created in the Money Supply

Graham suggests I am making a “minor” error, in stating that there is not enough money in the system to pay back the debt + interest. Let’s state this clearly; interest is not created in the money supply. It is added on top as an additional debt, for which there is no parallel money in the money supply, except in that you game it from another party. This is vital to understand. And if I were in error, it would certainly not be “minor.” The more money is leveraged and borrowed, the more impossible it is to pay back. And compound interest, which re-charges interest on money, is “even more impossible” (logical fallacies of that phrase aside.) It is no guarantee that the creditors Graham describes are spending their money back into the system (on what, we are not told); the borrower has paid back more than what was agreed knowingly (in the case or mortgages it’s often more than 100% more than what was borrowed to buy a house; and with wizardly new schemes like Wonga.com we are talking 1000% APR on admittedly very small “micro-loans”.)

Taken in aggregate, the total money supply of a given economy is in fact dwarfed by the debts, meaning a moving wall of defaults and corruption, as the impecunious masses compete and game each other for the rising costs to pay back inflating loans. Last one past the post would be bankrupted, or might end up in prison, where, without a shred of irony, he or she would “pay their debt to society.”

Graham moves on; he relates my point that I mention “with some disdain that a millionaire can earn £50k interest “simply by having money in an account with 5% interest rate”.” I apparently ignore “that (in a free market system, at least) the millionaire must have previously produced so much to satisfy the needs of his fellow man that he was able to become rich; that the money is not available to the millionaire during the time it is loaned out; that some risk is involved in lending; and most importantly that debtors voluntarily accept the terms of their loan and therefore expect to benefit from the transaction – the loan is for mutual benefit. Any third-party using violence to prevent this kind of voluntary exchange would clearly be making both worse off by preventing the gain from trade being realised.”

I would love to address this point, however, readers will see that while I am called on my non-definition of money, Graham here requires to define what he means by “free market”, and that wonderful word “voluntarily”. I have a feeling he is defining money in this scenario as 100% backed by a precious resource, or receipt money. However, I will have to wait for his terms before I make any claim on his proposed model. Meanwhile I can make some general points that should apply to every monetary system;

Established Systems vs Disruptive Technologies

Any millionaire, or rich group of individuals, will want to maintain their status as the richest in a society. Otherwise what’s the point of striving to be rich? This means that new disruptive innovations such as mass cheap transit will be fought by the existing and incumbent transport owners, no matter if they have a “state monopoly” or whether it’s a private cartel (or a lone super-moneyed oligarch.) We are immediately hindered from solving problems, if instead a steady, cyclical “treatment” of a problem can be secured by those with the most economic clout. This is a central point to the competitive mentality of a society.

No recourse, no second option

What’s voluntary about having to borrow and become indebted? This is not a rhetorical question, I literally don’t understand nor can follow the logic (our disposition in this movement is that we should celebrate being wrong, for we “become right” in the process. Here I stand ready to be educated by “Mr Wright” – pun intended.)

Contributing Nothing

My point stands in Graham’s quoted text above. A system whereby you can earn money off money with no further contribution to a society belies Graham’s assertion that one must have been useful. Even if said millionaire has done very useful actions – the game is up. Now ever increasing money-aggregate can leverage more and more disproportionate wealth gaps. Those born into the society are, unless they are inheriting this self-referential money gain of course, from the outset holding the bad hand of a stacked deck. A deck you are “voluntarily” allowed to borrow from, returning more cards than you borrowed at the outset. In time, the most money can be made off money itself. Whence the willingness to invest it in something other than that with the greatest possible gain? I fail to see how regulation OR deregulation of a banking system could solve this money-to-more-money cyclical cancer, which renders actual life systems entirely secondary to the guaranteed profit cycle. I look forward to feedback, as ever.

Graham suggests that I have overlooked a point on interest – that the alternative is “no interest.” I am fully aware that interest is used as the incentive in lending. It’s just not relevant to my points that interest itself is unsustainable, stacks the deck, and produces an Ouroboros-like self-serving loop in the financial system. That usury laws exist (particularly within Islamic banking) 0nly underlines the point that whole societies have come to see interest as immoral, to the point of being sinful. Hardly a point against me, there. As for the rest of the paragraph, much is made of money’s “non-availability”, “free market” and many other terms that require me to ask Graham what he means by this.

Social Mobility and Inequality

Here’s where things start to become interesting, and where my opener on Locke really comes into play. Graham has locked onto the work of social scientists like Richard Wilkinson and Kate Pickett of the equality trust, and manages to dismiss the implications of the causal relationship of inequality with a host of social ills, which also affect the rich with a paragraph here, and a few in a related post, the opening admission of which is telling;

“Empirical evidence itself is of no use for understanding the effects of different norms relating to how resources are used – for that we need economics, and economics is a strictly axiomatic-deductive, i.e. non-empirical, science, as explained by Austrian economists such as Ludwig von Mises, Murray Rothbard and Hans Hoppe.”

I can see why The Equality Trust’s data is of no importance to him here, since, like with Hayek, “Scientism” is of little value to economics, which prefers to focus on assumptions about human behaviour instead. We have it in black and white, the non-association of the real world with the human discipline of economics – we are not to trust science in determining the function of society, we must base it on an “invisible hand of the market” (I am quoting Smith – Graham does not.) Apparently this will function better. I am not sure of the evidence for this.

However Graham then frog-leaps back to the hunter-gatherer days, suggesting that certain individuals in this low-tech society “by saving and implementing good new ideas – like creating wheelbarrows, ploughs and pots, […] enabled them to produce more with less effort. Individuals with wheelbarrows were now wealthier than the “have-nots” who didn’t have them. The consistent opponent of inequality would have to denounce this improvement to the material conditions of man on account that it creates a two-class society and breaks the condition of high equality.”

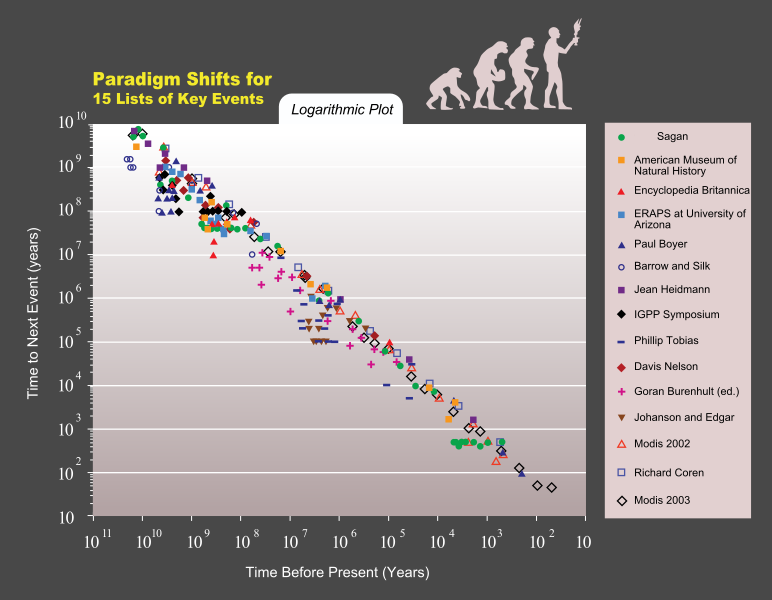

Ok – what were these individuals saving? We cannot emote the pre-monetary economies and then claim they are “saving” anything. Innovations, which by the way follow a very constant exponential increase (this link is below as a graph) since nature’s “invention” of RNA, then DNA, have never been purely enabled by money, and in fact pre-date money quite considerably. This is key – we use the current technology to create the next generation of technology. This is why we have this doubling. It transcends market-theories (except deliberate techno-primitivism, obviously.)

{kind=link}

Here’s a composite graph, with 15 separate lists of technologically notable events which all demonstrate this overarching trend :

Human ingenuity and material resources, both real-world attributes, are what enable innovation and technology (which includes wheelbarrows.) I would grant Graham the point that money became the tool to divide labour in a society facing real physical scarcity, but this does not grant money the noble title of being the enabler of technology. The technologies we create, to save labour, help us then create the next level of more complex technology. On and on it goes, until we start inventing not only technologies that disrupt the market (and are often suppressed to hold onto the aforementioned vested interests as I spend 40 minutes explaining here), but economics itself.

One cannot dismiss the application of science and technological development as important for the functioning of a society on one side, and yet claim the benefits of said developments as produced by a not yet existing economical system on the other. I WILL admit, once again, that there are forms of government which are often considered to be “anti-capitalistic” which got it completely wrong when trying to “centrally plan” – like Russia’s absurd Gosplan system, for example; but this is of course not at all what we propose. The logic of technological evolution is not aided by money. It was not begun by “saving”.

Additionally, Graham’s argument is internally inconsistent. What’s being valued here, by him, and by me, is the wonders of innovation. Yet the data from the Equality Trust shows that Innovation is higher in countries with less inequality (admittedly measured in patents filed – and while I’m no fan of patents, it does indicate quite well, in this system at least, the inventiveness on a national level – linked here too for clarity in case the image is too small):

We will ignore any moral arguments for caring for our fellow human beings for now – because this argument can be won without it. Hierarchically reinforced societies, with low social mobility, and/or a very large gap between rich and poor is bad for the very technology Graham is attempting to consign to the benefits of a monetary system.

Downsizing of Banks

I must be a very poor communicator indeed, for what I thought was a crystal clear example of how a monetary system (yes, any monetary system) weighs the human and natural world impact at zero, and wealth accumulation as most important is interpreted (and misunderstood) in complete reverse by Graham. First off, the loss of 45,000 jobs at Lloyds is an example of human well-being being placed second to the arbitrary effects of the gambling done by the Big Banks in the prior decades. Losing that many staff (who were either “made redundant” by reorganising workflows using technology, or had already been obsolescent) is a social cost of the bank preserving as much profit for itself as possible. The fact that the stock market goes UP in such cases is a plain example of the psychology of a system that counts its priorities only amongst numbers and has no relation to what John McMurtry has termed “The life-ground” – human individuals (which the Austrians seem otherwise to bang the drum for so incessantly), and the environment (more on that in a moment.) Graham also thinks that the loss of 45,000 jobs equates to a “downsizing of the banking sector” when in fact it is precisely the opposite. It is the GROWTH of the sector at the expense of 45,000 more individuals than were already impacted. Of course if you’re thinking in monetary terms it appears this way about, but the life-effects are in fact the opposite. Note here also a slight double-think. It’s good to replace jobs with automation, or at least with equal to greater output – we’re about to see Graham reject this idea when expressed directly.

Growth

Graham claims that I represent Growth = Good right after suggesting that growth per se is not necessarily good (this, I think, comes from the image on the screen at that point, which is a depiction of the assumption of the present banking and social zeitgeist, and so is evidently my fault for unhelpfully depicting it as if it were what I was asserting.) I’ll state clearly; an increase in technological ability, such as automation, data interpretation, construction efficiencies etc and life-indicators such as happiness, (Gross National Happiness or GNH actually is being advanced as an idea by some), health and life longevity-increases and so on are “good growth”. That is the central goal of the social model that we advocate. Humanity strives to better itself, a general rule I think is fair to pronounce. It is my position that these are hindered in the journey towards this by a competitive basis in society, in which one is restricted, and is in need of taking advantage of others to secure one’s position, meaning the detriment and social harm is “externalised” onto others. In truth, we are not going to survive unless all growth that our global society undergoes is literally sustainable within the biosphere. Anything else is like going into monetary debt – waste it now and live “beyond your means”, but it’ll come back to get you. The irony of course is, that efficient social organisation would mean vastly more for people. But this goes unspoken in our present paradigm, in which “value” is equated to restriction, conspicuous consumption, scarcity logic and so on.

Patents

In abstraction, patents are an expression of the market system. It is the securing of a certain technology, system, or idea, externally restricted (owned) by one or more people in order to maintain a competitive advantage. I do have a little trouble imagining how exactly a monetary system can function without any ownership or trademarked or copyrighted systems or products, if this abstract basis is considered; that is to say, a system which at its core requires ownership and will tend to monopoly or cartel behaviour (since this move ensures more security in the competitive environment.) Add to that the invisible societal cost of the progress we have NOT made because of patented battery technology that has hindered the development of an actually sustainable and functional electric car industry, and you begin to see why this is actually important for life on earth and technological progress, rather than for an abstract “market.” I’ll let Graham inform me of how this can be overcome.

Planned Obsolescence

This is a myth to Graham. His evidence is that the sovereign consumer is the all-powerful chooser of what s/he wishes to purchase, and those products with weak lifespans would be selected against. Almost a sort of market Darwinism.

Except of course that this is one of the very reasons why companies spend so much on advertising to retain and grow customers regardless of the product in question’s qualities. Were it not so, then all advertising would be truthful. On top of that, I’ll let the following iPhone4 breakage graph speak for itself:

Of course longevity is not the ONLY attribute. And physical manufacturing is also not the ONLY way in which obsolescence is made to bear. One of the best examples of this is the non-support of “outdated” software. All older phones (Apple or otherwise) will sooner rather than later be dropped from the software update support, forcing consumers to buy new phones. And since this is a general market force, there is nowhere to really turn to; for all companies require repeated as well as growing business. Companies are beholden to this as much as consumers are; that is, as long as cyclical profit cycles and earnings-profit-growth are the dominant market goals. Graham’s only alternative to this is interventionist “violence” (a word we are treated to again much later in his piece) to “force” companies to adhere to stringent rules to avoid this. In fact, we maintain that a shift from a competitive to a collaborative basis for social operation would vastly decrease the spiralling waste-consumption cycles we have become locked into in a bid to sell shit to each other quicker and more often, leaving 1700 phones an hour to be thrown into landfill just in the UK. Incidentally, The 15 million phones we upgrade every year in the UK contain a total of almost four tonnes of silver and 600kg of gold (what does that do to a Gold Standard I wonder half-seriously) not to mention arsenic and other poisons and heavy metals. Once again we underline the real “violence” here – towards ourselves and the planet.

If we ceased the competitive mentality and understood our actual place in the environment (a fact about which we have no choice – nature is in that sense a dictatorship), we wouldn’t have to “enforce” anything. All we are asking is that we apply real efficiency to our manufacturing, consumptive habits and to the design of items to be more than just throw-away. I’d even settle for a decrease of HALF of these depressing and needless statistics.

And to really put the nail in the coffin here; many people do not have the means to buy the products that really are much closer to the “best” one can manufacture at any given moment (this of course changes as our technology betters itself.) So the option to buy better is not guaranteed to many people. And once again, were such an item to be affordable, it’s only a matter of time before another company shaves off the manufactured efficiency or uses lower quality products and processes to undercut the competitor. Soon we are in a war of “monetary” efficiency, and the actual top-quality product has been reduced to complete non-availability, and duplicated, flawed and makeshift versions of what we consider a “mobile phone” or car or whatever, have flooded our landfills. But don’t worry! Wealth has evidently increased for some, hence we can defend this system of “consumption” (one can hear the medical term for that word more clearly when one considers the health risks at stake.)

The Ghost of an Ad Homiem – Technological Unemployment and Automation

Graham sneaks in an ad hominem against the “discredited” Keynes as if that entirely invalidates the point being made here (I am no explicit fan of his, by the way, and my arguments below actually do not rely on him – he just said it first – , but he didn’t exactly fail at The New Deal to clear up the mess of the prior “free market”, did he?)

Unfortunately Graham then rattles off a load of irrelevant points about Keynesian’s absurd policy towards “creating new work”. None of this is within the scope of what I was speaking about, or am about to speak about.

Stupid solutions to real problems do not make the real problems non-existent.

And while one can lay the blame of the 2008 crash on Keynes, one can always happily add Friedman and Hayek to that too – after all Hayek was pretty influential with Thatcher’s Britain, not to mention the Chicago Boys in the US, and Friedman’s own resulting work in Chile and Argentina (the retelling of which is often avoided by the defenders of the Free for all Market) speaks volumes about how “in the minority” these ideas in fact are, or what results from competitive and deregulated economic models.

Look; Labour-saving devices will ultimately outpace new job creation. Why? Well, as Artificial Intelligence begins to outstrip human intelligence (Ray Kurzweil places this at 2029, sometimes later) not only will we be able to automate almost every kind of endeavour, but the resulting unemployment will not provide the “market” to feed the industries that are now highly automated. Additionally, I should add, entire satellite industries will cease too because they are not “needed”. Amongst these are, purely off the top of my head, Human Resources (your workforce is mostly non-human, Travel Agents, Customer Service desks of almost every kind (a token few people here and there isn’t a replacement), Taxi drivers (only this week Google has pushed the self-driving car publicly since first announcing it, couching it in PR-friendly terms of being a “copilot”), that makes Lorry, bus and train drivers obsolete too. Marketing is increasingly reliant on IT for rapid audience-analysis, and advertising on the web really only picked up with Google (again), whose Adsense programme is an entirely semantically automated ad-placing industry.

The book that actually informs my position on this is The End of Work by economist Jeremy Rifkin. Without too much of a tangent in this direction, Rifkin actually foresees the voluntary industry (the “third sector) as becoming a major function of society as both spending power and employment become weaker in the market. I have no idea if this chimes in with the “Voluntaryism” with which Graham aligns himself. Once again, I will defer to him rather than guess my way through his ideas (something he unfortunately doesn’t hold back from with the solutions I propose – maybe I am expressing them poorly in the video.)

The process of automation is also sped up by the inevitable busts and crashes, as companies shave more and more off costs – and automation is cheaper due to efficiency and non-staffing benefits such as cyclical wages, illness, loss of concentration, limitations of the human frame in speed and exactness, as well as the complete avoidance of any labour laws, of course, including holiday and other labour gaps. And booms do not reverse the automated jobs.)

Perhaps it’s all too fanciful and unthinkable. Well, as one tiny isolated point on this, Foxconn is hiring 500,000 robot workers now to manufacture technology for practically every major consumer technology player on the globe. That’s up from 10,000. Any “need” to re-employ those workers, who are unskilled at worst, and skilled in only one thing at best, will not come from their requirement to eat. In fact, education itself is a big part of this. Education as China, and as Europe, has designed it, was designed to supply the very factory workers and lower-middle management that we are now replacing with automated labour (this point on education is actually made in a different Rifkin book, The Third Industrial Revolution.) We don’t have an appropriate educational system needed to retrain the displaced workers. And even if we did, we’re whistling past the graveyard on this one. Machine intelligence doubles every 8 months, human intelligence does not. The lines will intersect and cross each other. And at that point we will not be able to maintain a monetary-market system of any meaningful value.

This movement calls for the deliberate automation of as much as we can. We consider it socially irresponsible not to. Not to mention the efficiencies, improvements and possibilities for societal redesign that are natural corollaries to placing technology at the centre of our way of life. Work for work’s sake is asinine. On this point Graham and I agree. As for his undeveloped assertion that if people didn’t have to work for a living, this is not a scientifically or historically sound assumption. Human beings do not need to be coerced into action. Drive, by Daniel Pink, while being overtly a manual for new management approaches, is in fact a brilliant collection of studies ranging as far back as Edward Deci and others, who demonstrated through testing and research (rather than guesswork based on econo-axiomatic assumptions) that creative work is hindered by promised or expected monetary gains, and that money only affects those jobs positively that are mechanical, and can be sped up by human subjects without running the risk of doing the job poorly; in other words the very jobs we can now automate. The end of work, as Rifkin put it, does not rely upon “authorities” such as Keynes or anyone else. It relies on what comprises human ability, and what we can do with our technology. It should be celebrated and promoted. Yet, in a monetary system, it is very much to be feared. How long before your skill-set (and mine) is dwarfed by faster, cheaper, better technologies? How long will you still have the capacity to retrain as we advance ever quicker, doubling our technical powers of computing every year? Not long; and no amount of Brow-Beating by Mises in his “Anti-capitalistic Mentality” that the market has shown up my weaknesses, and that’s in fact what I’m frustrated about, will satisfy the real-world trends.

Mises was a very gifted Capitalistic theorist. However, I’d love to see him confronted with today’s technology and how the trends have played out. Also our use of advertising, a coercive market technique, didn’t exist at all in their form when he was writing. PR was invented after World War II, and traded on our ability to be manipulated into astonishing irrationality. I wonder if he would have revised his theories. A brilliant mind such as his may well have done, given the new information. And brilliant minds are always happy to do so. We’ll never know.

The Ghost of Marx (my final point for now)

Unfortunately Graham misunderstands how technology develops, misattributes me (indirectly) to Marx here, and is confusing invention with overall technological progress. In fact, my point here comes back to Ray Kurzweil once again, and something called The Law of Accelerating returns. It is by no means a howler. The only howler here once again MUST be my failure in the allotted time to delve into this topic clearly enough. My apologies Graham. Here is the contour of what I was trying to explain:

Our ability to create more powerful technologies (both good and ill unfortunately) DO NOT depend on a market system, or the freedom of human beings per se. As I have stated previously, we use the technology we have at our disposal, and the abilities which that technology disposes us towards. The scribes you mention, for example, could not have printed anything with the quality I can in my own room without any skill. No amount of “freeness” on their part would change this. Consider, it took humanity 15 years to sequence the genes of the AIDS virus. In comparison, SARS was sequenced in 31 days, and modern “over the internet counter” sequencing services can now sequence a genome in a single day for multiple people. Is this because humanity is “more free” than before? Well, obviously not. This is all I was trying to express. Our abilities are as good as our technology. And our abilities now are awe-inspiring (if we’re lucky enough to be using the technology in life-preserving ways) and terrifying (if we instead decide to use them to destroy each other.) And it is this trend towards rapid, constantly disruptive technological ability, and all its effects upon employment, longevity, general health and possible uses towards a clean environment that has developed since nature created RNA and then DNA, all the way through the invention of money, and will survive in a post-money economy too.

In my second post I will focus on what a Resource Based Economy is, as well as address his points on energy, and the remaining unaddressed points. This will be a useful lumping together since the last half of his critique hinges only on the briefest of explanations by me, originally intended to be a call to “go and research the larger idea”, if you like. And I can tell you right now that “central planning”, voting in “supermen” and enforcing the system through violence, all hallmarks of a prima facie characterization based on a few minutes of my video and nothing else, will be rapidly be debunked and are, by the very logic of the system that is emerging all by itself, in utter contradiction to what it means to live equitably and sustainably on the planet in an intelligently managed and genuinely harmonious way.

It is not perfect – but perfect doesn’t exist.

Once again, I will give Graham the benefit of the doubt in this, and suggest as I did at the beginning that his misunderstanding are my fault, and not his – while reminding him that the books on Austrian Economics and Libertarian Ideology grow by the day on my shelf; we shall see if the writings of Jacque Fresco, Buckminster Fuller, Ray Kurzweil, Carl Sagan, Wilkinson & Picket or others, grow on his in the meantime, and inform his world-view.

After all, that’s what a rational discussion has to be about.

Pingback: Resource Based Economy | Pearltrees

Pingback: Explaining the Resource Based Economic Train of Thought | The Zeitgeist Movement – UK